![]()

General Questions

1.

Q:

What is Pillar Two Portal?

A:

Pillar Two Portal is a system designated by the Commissioner of Inland Revenue under Part 4AA of the Inland Revenue Ordinance (Cap. 112) ("the Ordinance") for Part 4AA entities to submit top-up tax notifications, file top-up tax returns to the Inland Revenue Department ("the Department"), and view and/or download top-up tax assessments issued by the Department. The Pillar Two Portal is an extended part of the Business Tax Portal ("BTP"). After registration with BTP, Part 4AA entities can access the Pillar Two Portal directly from the BTP.

2.

Q:

Should the Part 4AA entity register for a Pillar Two Account in order to access to the Pillar Two Portal?

A:

Separate registration for a Pillar Two Account is not required. Business Tax Portal ("BTP") Administrators of the Part 4AA entity / Authorized Users who are assigned to handle Pillar Two Matters on behalf of the Part 4AA entity can access the Pillar Two Portal directly from the BTP.

For User Guides and e-Demos about the access of Pillar Two Portal from the BTP, please visit the Pillar Two Portal Resource Centre Page.

3.

Q:

Can a Part 4AA entity engage a service provider for top-up tax reporting purposes and what matters can the service provider handle?

A:

Yes. A Part 4AA entity can engage a service provider to handle all matters under the Pillar Two Portal through the Business Tax Portal ("BTP") and should notify the Department of such engagement when the Part 4AA entity sets up or updates its profile of the BTP Business Account. The designated service provider can engage the client under the Tax Representative Portal and access the Pillar Two Portal directly.

4.

Q:

I am a service provider engaged under section 13 of Schedule 63 to the Ordinance. How can I access the Pillar Two Portal?

A:

You have to register for a Tax Representative Portal ("TRP") Business Account. Before registering for a TRP Business Account, you must have a registered Business Tax Portal ("BTP") Business Account with BTP Administrator(s) appointed. After registration with TRP, you can engage the client for handling Pillar Two matters and access the Pillar Two Portal directly.

For User Guides and e-Demos about the access of Pillar Two Portal from the TRP, please visit the Pillar Two Portal Resource Centre Page.

5.

Q:

I am the person who acts for, or is responsible for the management of the Part 4AA entity ("PRM"), that is not a corporation, under section 36(1) of Schedule 63 to the Ordinance. How can I access the Pillar Two Portal?

A:

First of all, the Part 4AA entity should provide details of its PRM through the Business Tax Portal ("BTP") when the Part 4AA entity sets up or updates its profile of the BTP Business Account.

For an individual PRM, you can access the Pillar Two Portal through the Part 4AA entity’s BTP Business Account directly.

For a corporate PRM, please refer FAQ 4 above.

6.

Q:

Will there be user guides / guiding screens on how to access the Pillar Two Portal?

A:

Yes, please visit the Pillar Two Portal Resource Centre Page for the User Guides and e-Demos.

7.

Q:

What should I do if the Part 4AA entity does not have a Business Registration Number ("BRN") to register for a BTP Business Account?

A:

To register a Business Account under Business Tax Portal ("BTP"), the responsible person performing the registration is required to input, among others, the BRN of the Part 4AA entity. In general, a Part 4AA entity should have a BRN if it carries on business in Hong Kong. If the Part 4AA entity currently does not have a BRN but has the obligations to apply for a business registration certificate, it should approach the Business Registration Office of the Department directly to complete business registration procedures before performing any online registration of the BTP Business Account. If the Part 4AA entity is not carrying on any business in Hong Kong but wishes to register a BTP Business Account to fulfill its reporting obligations, it should write to IRD via beps2.0@ird.gov.hk to request for a Business Registration Number Equivalent ("BRNE"), which will serve the function of the BRN for the purpose of registration with the BTP, by providing the following information:

- the reason why the Part 4AA entity is not required to apply for a business registration certificate in Hong Kong;

- name and Hong Kong Identity Card Number of the responsible person of the Part 4AA entity; and

- whether the Part 4AA entity is a corporation or not.

8.

Q:

Can a Part 4AA entity authorize a tax representative for the purposes of global minimum tax and Hong Kong minimum top-up tax and what matters can the authorized representative handle?

A:

Yes. Part 4AA entity can authorize a tax representative to handle Pillar Two matters through the Business Tax Portal ("BTP") and notify the Department of such authorization when the Part 4AA entity sets up or updates its profile of the BTP Business Account. The designated tax representative can, through the Tax Representative Portal ("TRP"), make enquiries relating to Pillar Two matters, and lodge objections against top-up tax assessments on behalf of the Part 4AA entity. Please also refer to FAQ 9 below.

9.

Q:

A Part 4AA entity has authorized me as its tax representative to handle Pillar Two matters when it set up its account profile. Can I access the Pillar Two Portal and submit a top-up tax notification/top-up tax return for the Part 4AA entity?

A:

A tax representative, if not engaged as a service provider of the Part 4AA entity under section 13 of Schedule 63 to the Ordinance, is not allowed to file a top-up tax notification/top-up tax return on behalf of its client. However, the tax representative can view the top-up tax notification/top-up tax return already filed under the Pillar Two Portal, make enquiries and lodge objections against top-up tax assessments under the Tax Representative Portal.

![]()

10.

Q:

How does the Pillar Two Portal authenticate the identity of the person conducting transactions under the Pillar Two Portal?

A:

For conducting transactions under the Pillar Two Portal, such as submission of a top-up tax notification and filing of a top-up tax return, the Part 4AA entity, service provider or person managing the non-corporate Part 4AA entity is required to use an e-Cert (Organisational) with AEOI Functions for authentication. For more information about e-Cert (Organisational) with AEOI Functions, please click here to visit the website of the Hongkong Post Certification Authority.

11.

Q:

I am a holder of an e-Cert (Personal). Can I use that digital certificate for authentication under the Pillar Two Portal for the Part 4AA entity?

A:

No. An e-Cert (Organisational) with AEOI Functions must be used. The e-Cert (Personal) cannot be used for authentication under the Pillar Two Portal for the Part 4AA entity. Each authorized person, when conducting transactions under the Pillar Two Portal, must hold the relevant organisation’s e-Cert (Organisational) with AEOI Functions issued by the Hongkong Post Certification Authority.

12.

Q:

The Part 4AA entity is an existing subscriber of an e-Cert (Organisational). Can that digital certificate be used for authentication under the Pillar Two Portal for the Part 4AA entity?

A:

No. An e-Cert (Organisational) with AEOI Functions must be used. An e-Cert (Organisational) is not accepted by the Pillar Two Portal for authentication. The Part 4AA entity may choose to add the new feature of AEOI functions when renewing the existing certificate. For further details of the procedures and documents required, please click here to visit the website of the Hongkong Post Certification Authority.

13.

Q:

The Part 4AA entity has subscribed an e-Cert (Organisational) with AEOI Functions for submitting CbC Return to the CbC Reporting Portal. Can that digital certificate be used for authentication under the Pillar Two Portal for the Part 4AA entity?

A:

Yes. The Part 4AA entity can use the same e-Cert (Organisational) with AEOI Functions for authentication under the Pillar Two Portal. It is not required to apply for another digital certificate.

![]()

14.

Q:

What should I do if I forgot the password of my e-Cert (Organisational) with AEOI Functions?

A:

In case you forgot your password, you are recommended to revoke your e-Cert (Organisational) with AEOI Functions immediately and apply for a new one. For more details, please contact the Hongkong Post Certification Authority direct.

![]()

Filing of Top-up Tax Notification

15.

Q:

Which entity is required to file a top-up tax notification for a fiscal year?

A:

A Part 4AA entity of an in-scope MNE group for a fiscal year is required to file top-up tax notifications for that year. As defined in section 1(1) of Schedule 63 to the Inland Revenue Ordinance (Cap. 112), a Part 4AA entity, in relation to an MNE group, means ─

(a) a HK constituent entitiy;

(b) a HK standalone JV;

(c) a HK member of a JV group; or

(d) a Part 4AA stateless constituent entitiy.

16.

Q:

Can an in-scope MNE group appoint one entity to file a top-up tax notification on behalf of the group?

A:

Yes. If a HK constituent entity ("HKCE") has filed a top-up tax notification in respect of an in-scope MNE group for a fiscal year and identified itself as the ultimate parent entity, the designated filing entity, or the designated local entity of the group, other HKCEs of the group are not required to file top-up tax notifications for that year. Similarly, if a HK member of a JV group has filed a top-up tax notification in respect of a JV group for a fiscal year and identified itself as the designated local entity of the JV group of the in-scope MNE group, other HK members of the JV group are not required to file top-up tax notifications in respect of the same JV group of the MNE group for that year.

However, a HK standalone JV and a Part 4AA stateless constituent entity must file its own top-up tax notification.

17.

Q:

A HK member of a JV group of an in-scope MNE group is also a HK member of a JV group of another in-scope MNE group. Should the entity file a top-up tax notification in respect of each MNE group?

A:

Yes. A top-up tax notification should be filed in respect of each MNE group.

18.

Q:

How can a Notifying Entity file a top-up tax notification?

A:

The top-up tax notification should be filed through the Pillar Two Portal. For details, please refer to A Guide to Submit Top-up Tax Notification.

19.

Q:

Is there any registration requirement before a Notifying Entity can file a top-up tax notification?

A:

20.

Q:

If an ultimate parent entity of an in-scope MNE group and / or a joint venture of a JV group is not located in Hong Kong and the jurisdiction in which it is located does not issue a Tax Identification Number, in completing Form IR1485, what should be inputted as "Business Registration Number / Tax Identification Number" in Item 4(b)(iii) under Part 2 and / or Item 2(c) under Part 3 of the form?

A:

Please input "NOTIN" in Item 4(b)(iii) under Part 2 and / or Item 2(c) under Part 3 of Form IR1485.

21.

Q:

When accessing a top-up tax notification under the Pillar Two Portal, the Notifying Entity has to input the Business Registration Number / Tax Identification Number ("TIN") of the Ultimate Parent Entity ("UPE") / Joint Venture ("JV"). If the UPE and / or the JV is not located in Hong Kong and the jurisdiction in which it is located has not issued a TIN to it, what should be inputted?

A:

"NOTIN" should be inputted as "Business Registration Number / Tax Identification Number of the Ultimate Parent Entity" and / or "Business Registration Number / Tax Identification Number of the Joint Venture".

22.

Q:

A Notifying Entity is required to provide particulars of all HK constituent entities / HK members of JV group of the in-scope MNE group in Part 3 of a top-up tax notification. How can the information be provided?

A:

In completing a top-up tax notification on the Pillar Two Portal, the Notifying Entity can provide details of all HK constituent entities or all HK members of the JV group by either online input or upload a CSV file. The CSV file should be prepared in advance, containing business registration numbers of the entities, and should be saved in UTF-8 ".csv" format. The system will reject the CSV file, which is not UTF-8 encoded. For details, please refer to A Guide to Submit Top-up Tax Notification.

23.

Q:

Can a Notifying Entity make any amendments to a top-up tax notification which has been submitted through the Pillar Two Portal?

A:

i. the list of Hong Kong constituent entities of the MNE group; or

ii. the list of Hong Kong members of the JV group.

![]()

24.

Q:

A:

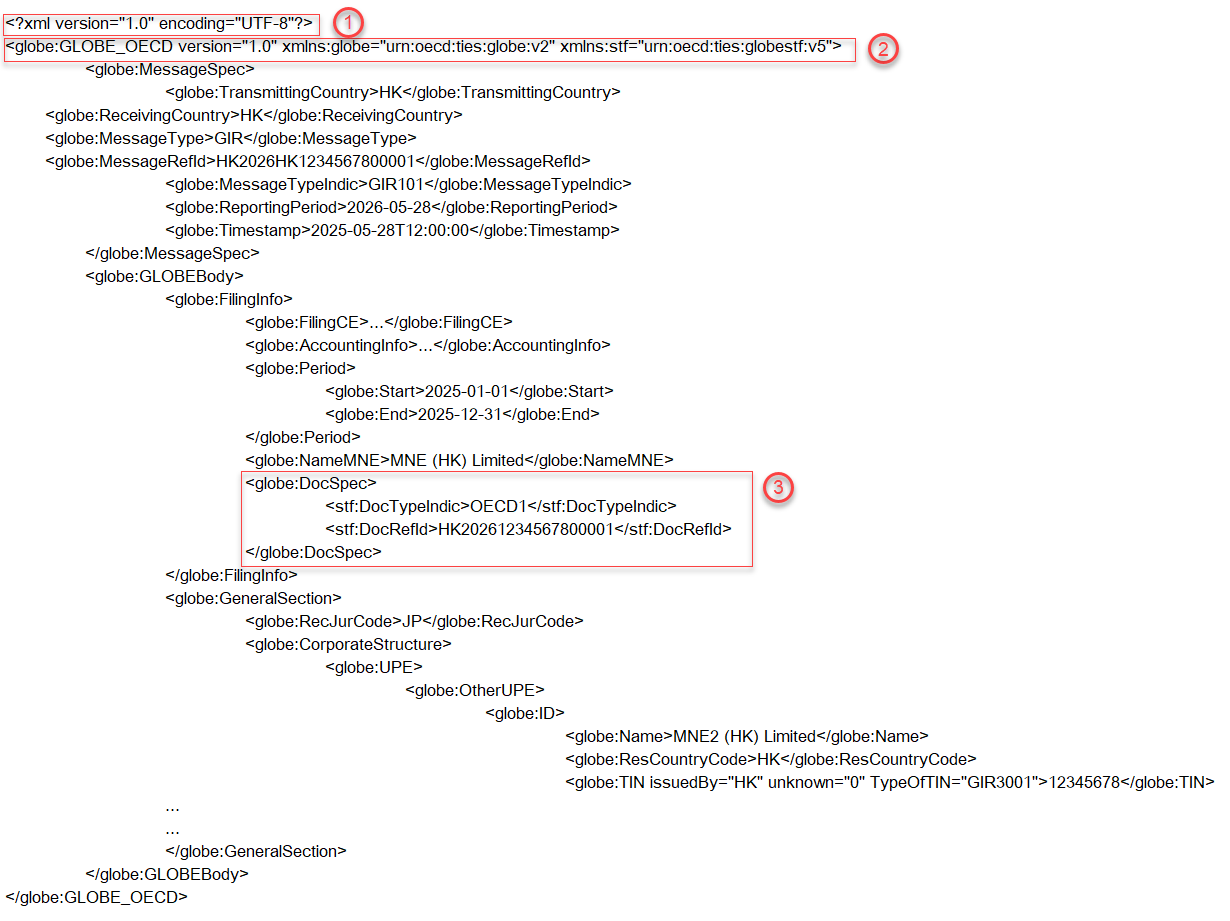

A data file should be prepared in the Extensible Markup Language (XML) format, which is set out in the GIR XML Schema and user guide published by the Organisation for Economic Co-operation and Development, and the supplementary user guide published by the Department for preparing the GIR data file to the Department. For details, please refer to the GIR XML Schema and User Guides.

25.

Q:

A:

![]()

26.

Q:

How can I check whether a data file conforms to the requirements of the GIR XML Schema and the relevant user guides?

A:

Data file should be prepared in accordance with the requirements of the GIR XML Schema and the relevant user guides. The Encryption Tool provided by the Department would perform schema validation during the encryption process. Test data file can be submitted to the Pillar Two Portal for validation.

27.

Q:

How can I encrypt the data file containing GIR information?

A:

An Encryption Tool has been provided in the Pillar Two Portal. With your e-Cert (Organisational) with AEOI Functions, you can use the Encryption Tool to encrypt the data file.

28.

Q:

What if I have mistakenly submitted my production data file to the Pillar Two Portal via the "Submit Test Data File" function?

A:

Data file uploaded here will be tested for its conformity with the data specifications of GIR XML Schema. The test data will not be treated as GloBE information return to be filed by a Filing Entity. To protect your own data, please do not give actual data of the in-scope MNE group for testing.

29.

Q:

Is there any information required to be inputted when encrypting a data file with the Encryption Tool provided by the Department?

A:

No. Number of data elements including FilingInfo, GeneralSection, Summary, JurisdictionSection and UTPRAttribution in the data file will be displayed for checking when encrypting a data file with the Encryption Tool. You will not be prompted to input such information.

![]()

![]()