|

|

|

| |

|

| Assessing Functions |

| |

| |

The Department raises revenue through taxes, duties and fees in accordance with the relevant legislations. While the duties and fees collected for a year are based on the actual results of the year, the Earnings and Profits Tax assessed are principally computed by reference to the incomes/profits of the taxpayers in the previous year. For 2004-05, the Earnings and Profits Tax assessed increased by $18 billion (21%), as compared with the previous year. The total of duties and fees collected also rose by 20%. |

|

| Profits Tax |

| |

Profits Tax is levied on individuals, corporations, bodies of persons and partnerships, in respect of assessable profits arising in or derived from Hong Kong. For the year of assessment 2004-05, the Profits Tax rate for corporations remained unchanged at 17.5% and the rate for non-corporate persons was increased from 15.5% to 16%.

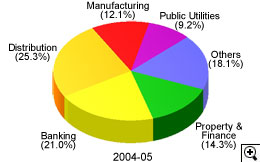

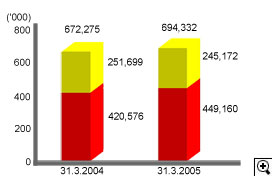

With the economic upturn, Profits Tax assessed in 2004-05 increased by $11.1 billion (21%), as compared with the previous year. Total Profits Tax assessed during the year amounted to $64.2 billion (Figure 5) . Of the total tax assessed, the property and financial sectors together contributed 35.3% (Figure 6) . Further statistics relating to the tax assessed in respect of different business sectors are shown in Schedules 3 and 4.

|

| |

|

| |

| Salaries Tax |

| |

Salaries Tax is charged on all income arising in or derived from Hong Kong from any office (e.g. a directorship), employment or pension. The total tax payable is restricted to an amount not exceeding the standard rate of Salaries Tax of the net total income (without allowances) of the individual concerned. For the year of assessment 2004-05, the standard rate was increased from 15.5% to 16%.

Compared to the previous year, while the number of assessments made remained very much the same, 23% more tax was assessed during 2004-05 (Figure 7) . Analyses of tax assessed and allowances granted in respect of taxpayers at various income levels are provided in Schedules 5 and 6. |

| |

|

|

Following the implementation of phase I tax increase measures in the 2003-04 Budget, the number of standard rate taxpayers increased by 15,032, from 11,697 last year to 26,729 this year. These taxpayers together contributed 31.8% of the Salaries Tax assessed, compared to 20.2% last year (Figure 8) . |

|

|

| |

| Notification Requirements of Employers |

| |

Apart from reporting commencements and cessations of employments, employers are required to prepare annual returns to report the emoluments of each of their employees. During the year, 228,280 employers filed employer's returns with the Department.

The Department provides venues for e-Seminar and disseminates tax information for employers on the IRD Homepage in order to enhance their understanding of the relevant statutory requirements. The contents include information about completion of Employer's return, employer's obligation, answers to frequently asked questions etc.. Employers can also obtain specimens of completed employer's returns and notifications through the Fax-A-Form service. |

| |

|

| |

|

| |

| Property Tax |

| |

Property owners (including corporations) are subject to Property Tax which is charged at the standard rate (up from 15.5% to 16% for the year of assessment 2004-05) in respect of the net assessable value of the property. Incorporated and unincorporated businesses that pay Property Tax in respect of their business premises can have such payments set off against their Profits Tax liabilities. As for corporations, income arising from properties owned by them is also subject to Profits Tax at the corporate tax rate. To obviate the need for yearly set-off of Property Tax against Profits Tax, a corporation can apply for exemption of Property Tax on the property concerned. Statistics on the classification and ownership of properties, based on the records of the Department, are provided in Schedule 7. As compared with the previous year, the number of assessments made during the year increased slightly by 1.9% while the amount of Property Tax assessed dropped by 2.3% (Figure 9) . |

|

|

| |

|

|

| |

Number |

Tax assessed |

|

|

|

| |

|

| |

| Personal Assessment |

| |

An individual may elect Personal Assessment in respect of his or her total income. Under Personal Assessment, all of the income of the taxpayer and his or her spouse is aggregated and, after the deduction of all allowances, is assessed at the graduated tax rates. In appropriate circumstances, this reduces the total tax liability of the individual (e.g. an individual who would otherwise be chargeable at the standard rate on each separate income source). As a result of an increase in the number of elections, the number of assessments made in 2004-05 was 1.3% more than the previous year. The amount of tax assessed increased by 8.7% (Figure 10) . |

| |

|

|

| |

Number |

Tax assessed |

|

|

|

| |

|

| |

| Advance Ruling |

| |

The advance ruling service allows a person to apply for a ruling on how a provision of the Inland Revenue Ordinance applies in relation to a particular arrangement.

A fee is charged for the service on a "cost recovery" basis. Initially, the applicant is required to pay an application fee of $30,000 for a ruling concerning the "Territorial Source Principle", or $10,000 for a ruling on any other matter.

The Department endeavours to provide a ruling within 6 weeks of the date of application, provided that all relevant information is furnished with the application and further consultation with the applicant is not required.

During the year, 77 advance ruling applications were processed (Figure 11) . Most of the applications were for rulings on Profits Tax matters. |

| |

|

| |

|

|

2003-04 |

2004-05 |

| |

|

Number |

Number |

| Awaiting decision at the beginning of the year |

|

9 |

|

19 |

| Add: |

Applications received during the year |

|

90

|

|

71

|

| |

|

|

99 |

|

90 |

| Less: |

Disposed of - |

|

|

|

|

| |

Ruling made |

70 |

|

66 |

|

| |

Application withdrawn |

4 |

|

7 |

|

| |

Ruling declined |

6

|

80

|

4

|

77

|

| Awaiting decision at the end of the year |

|

19

|

|

13

|

|

| |

|

| |

| Objections |

| |

| A taxpayer who is aggrieved by an assessment made under the Inland Revenue Ordinance may lodge an objection to the Commissioner. A significant proportion of the objections received each year arise from estimated assessments issued to taxpayers who have failed to lodge returns on time. An objection of this nature must be supported by a completed return and, where applicable, by supporting accounts. Most of these objections are settled promptly by reference to the returns subsequently submitted. Many of the other types of objections are also settled by agreements between the taxpayers and the assessors concerned. Relatively few objections are ultimately referred to the Commissioner for determination. During the year, the Department processed over 73,000 objections (Figure 12) . |

|

| |

|

| |

|

|

2003-04 |

|

|

|

Number |

|

| Awaiting settlement at the beginning of the year |

|

24,499 |

|

26,418

|

| Add: |

Received during the year |

|

68,961

|

|

71,654

|

| |

|

|

93,460 |

|

98,072

|

Less: |

Disposed of - |

|

|

|

|

| |

Settled or withdrawn |

66,094 |

|

72,838 |

|

| |

Assessment confirmed |

540 |

|

496 |

|

| |

Assessment reduced |

253 |

|

228 |

|

| |

Assessment increased |

142 |

|

128 |

|

| |

Assessment annulled |

13 |

67,042

|

28

|

73,718

|

| Awaiting settlement at the end of the year |

|

26,418

|

|

24,354

|

|

| |

|

| |

| Appeals to the Board of Review |

| |

| A taxpayer who is dissatisfied with the Commissioner's determination of his objection may appeal to the Board of Review (independently set up under the Inland Revenue Ordinance) to have the determination reviewed. As at 31 March 2005, the Board consisted of a chairman and 9 deputy chairmen, who have legal training and experience, as well as 119 other members. During the year, the Board processed 166 appeals (Figure 13) . |

|

| |

|

| |

Number |

| Awaiting hearing or decision as at 1 April 2004 |

|

101 |

| Add: |

Lodged during the year |

|

149

|

| |

|

|

250 |

Less: |

Disposed of - |

|

|

| |

Withdrawn |

42 |

|

| |

Assessment confirmed |

76 |

|

| |

Assessment reduced in full |

5 |

|

| |

Assessment reduced in part |

37 |

|

| |

Assessment increased |

3 |

|

| |

Assessment annulled |

3

|

166

|

| Awaiting hearing or decision as at 31 March 2005 |

|

84

|

|

| |

|

| |

| Appeals to the Courts |

| |

|

A decision of the Board of Review is final, provided that either the taxpayer or the Commissioner may, pursuant to section 69(1) of the Inland Revenue Ordinance, make an application requiring the Board to state a case on a question of law for the opinion of the Court of First Instance.

During 2004-05, the Court of First Instance ruled on five cases relating to the Inland Revenue Ordinance. Decisions in favour of the Commissioner were given by the Court in respect of appeals concerning the taxability of profits from the sale of property, the source of trading profits, a refusal of the Board to grant an extension of time to allow a taxpayer to appeal against a determination of the Commissioner, and the taxability of royalties. Appeals to the Court of Appeal have been lodged in respect of the latter two decisions. In a case concerning the taxability of termination payments received by an employee, an appeal by the Commissioner against the decision of the Board was partially allowed by the Court.

During the year, the Court of Appeal handed down one decision, in favour of the Commissioner, relating to the Ordinance. The case was concerned with the issue of whether the provisions of the Ordinance concerning personal assessment in the case of a married couple were inconsistent with the Basic Law.

The Court of Final Appeal also handed down a decision relating to the Ordinance. The case involved the issue of whether fees in respect of an underwriting contract relating to the sale of property in the Mainland of China were chargeable to Profits Tax. The Court found in favour of the Commissioner.

Figure 14 sets out statistics concerning appeals to the Courts for 2004-05. |

| |

|

| |

|

|

Court of

First Instance |

Court of

Appeal |

Court of

Final Appeal |

|

| Awaiting hearing or decision as at 1 April 2004 |

|

17 |

|

1 |

|

1 |

19 |

| Add: |

Lodged during the year |

|

20

|

|

4

|

|

-

|

24

|

| |

|

|

37 |

|

5 |

|

1 |

43 |

| Less: |

Disposed of - |

|

|

|

|

|

|

|

| |

Decided |

5 |

|

1 |

|

1 |

|

|

| |

Discontinued |

10

|

15

|

-

|

1

|

-

|

1

|

17

|

| Awaiting hearing or decision as at 31 March 2005 |

|

22 |

|

4 |

|

0 |

26

|

|

| |

|

| |

| Business Registration |

| |

The Department aims to maintain an efficient business registration system. Every person carrying on business in Hong Kong must register the business and pay the required fee. Registered businesses may renew their registration certificates either annually or once every 3 years. The registration fee and levy for the Protection of Wages on Insolvency Fund are respectively $2,000 and $600 if paid annually, or $5,200 and $1,800 if paid every three years. Up to 31 March 2005, 10,046 businesses had taken the 3-year certificates.

The Department aims to maintain an efficient business registration system. Every person carrying on business in Hong Kong must register the business and pay the required fee. Registered businesses may renew their registration certificates either annually or once every 3 years. The registration fee and levy for the Protection of Wages on Insolvency Fund are respectively $2,000 and $600 if paid annually, or $5,200 and $1,800 if paid every three years. Up to 31 March 2005, 10,046 businesses had taken the 3-year certificates.

As the economy was picking up, the total number of new and re-opened registrations in 2004-05 was 12,704 higher than that of the previous year while the number of cancelled registrations increased slightly by 1,484 (Schedule 8). The total number of active registrations recorded a growth of 22,057 for the year (Figure 15) . There was a corresponding increase in the number of certificates issued, leading to an increase of $115 million in the business registration fees collections (Figure 16) . |

|

| |

| |

|

2003-04 |

2004-05 |

Increase |

Number of certificates issued (Main and Branch) |

712,934 |

733,825 |

2.9% |

Fees (inclusive of penalties) ($m) |

1,233.3 |

1,348.7 |

9.4% |

|

| |

Under the Business Registration Ordinance, a small business with average monthly sales or receipts below a specified limit ($10,000 for a business mainly deriving profits from the sale of services or $30,000 for other businesses) could apply for exemption from payment of the fee and levy. The number of total exemptions granted during the year was 15,924, representing an increase of 16% from the previous year.

Where an application for exemption is not allowed, the business operator may appeal to the Administrative Appeals Board. 8 appeals were received by the Board in 2004-05, of which 6 were subsequently withdrawn by the appellant (Figure 17) . |

| |

|

| |

|

|

|

Number |

| Awaiting hearing as at 1 April 2004 |

|

1 |

| Add : |

Lodged during the year |

|

8

|

| |

|

|

9 |

| Less : |

Disposed of |

|

|

| |

Appeal dismissed |

0 |

|

| |

Appeal withdrawn |

6

|

6

|

| Awaiting hearing as at 31 March 2005 |

|

3

|

|

|

|

|

| |

|

| |

| Stamp Duty |

| |

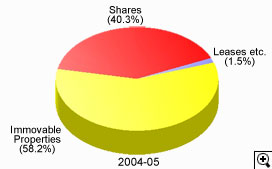

Stamp Duty is charged on instruments effecting property and stock transactions and leasing of property (Figure 18) .

As a result of the active property market in 2004-05, especially for luxury flats, the stamp duty collections from property transactions increased sharply by 85% when compared with the previous year.

With the rebounding economy, there was also a 6% rise in stamp duty collections from share transactions.

Overall, there was a handsome increase of 41% in total stamp duty collections during the year (Figure 19 and Schedule 9) . The number of documents stamped, however, dropped slightly by 1% (Schedule 10) . |

|

|

| |

|

| |

|

|

2003-04 |

2004-05 |

Increase |

|

( $m ) |

( $m ) |

|

Immovable Properties |

4,996 |

9,233 |

+85% |

Shares |

6,019 |

6,388 |

+6% |

Leases etc. |

230 |

230 |

0% |

Total |

11,245 |

15,851 |

+41% |

|

| |

|

| |

| Estate Duty |

| |

Estate Duty is charged on that part of a deceased person's estate situated in Hong Kong. The threshold for levying duty is $7.5million and the duty rates range from 5% to 15%, depending on the value of the estate.

|

Figures 20 and 21 show the composition of estates and cases processed for the past two years.

|

|

|

| |

|

|

| |

| |

2003-04 |

2004-05 |

| New cases |

15,654 |

16,064

|

| Cases finalised |

|

|

| |

Dutiable |

258 |

271 |

| |

Exempt |

15,362

|

15,660

|

| |

15,620

|

15,931

|

|

|

Estate Duty of $1.468 billion was collected during the year (Schedule 11), an increase of $13 million (0.9%) compared with that of the previous year.

Estate Duty is payable on delivery of an estate duty affidavit or account (or within 6 months from the date of the deceased's death, whichever is the earlier). $1.265 billion was received during the year in advance of the issue of formal assessments (Schedule 12) . |

| |

|

| |

| Betting Duty |

| |

Betting Duty is charged on bets made on totalisators at race meetings conducted by the Hong Kong Jockey Club, on the proceeds of lotteries conducted by the HKJC Lotteries Limited and on the net stake receipts from the conduct of authorised betting on football matches by the HKJC Football Betting Limited.

In 2004-05, the rates of duty remained unchanged (Figure 22) . |

| |

|

| |

|

|

Rate |

Standard Bets |

win, place, double, quinella and quinella place |

|

Exotic Bets |

six up, treble, tierce, trio, double trio and triple trio |

|

Lotteries |

|

|

Football Betting |

|

|

|

| |

| Note: |

* Overseas bets are charged at 6%.

**Duty rate on the net stake receipts. |

| |

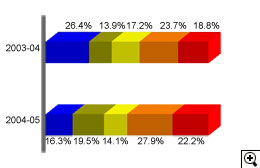

During the year, both the racing attendance and bets on horse racing were on the decline (Schedule 13) , resulting in a drop of 8.6% in the duty collected from horse racing. This was, however, compensated by a sharp increase of 88.3% in football betting duty collections and a 22.9% increase in lotteries duty collections. Total betting duty collections in 2004-05 was 3.6% higher than the previous year (Figure 23) . |

| |

|

| |

| |

2003-04 |

2004-05 |

Increase/Decrease |

| |

($m) |

($m) |

|

| Horse Racing |

9,258.7 |

8,466.7 |

-8.6% |

| Lotteries |

1,352.9 |

1,662.2 |

+22.9% |

| Football Betting # |

1,024.3 |

1,928.3 |

+88.3% |

| Total |

11,635.9 |

12,057.2 |

+3.6% |

|

| |

| Notes: # Football Betting Duty was introduced in August 2003. |

| |

|

| |

| Hotel Accommodation Tax |

| |

Hotel Accommodation Tax is imposed on hotel and guesthouse accommodation at the rate of 3% of the accommodation charges paid by guests and is collected quarterly in arrears.

In 2004-05, there was an increase in the number of hotels, boarding houses and taxable rooms (Figure 24) . Due to the growing number of visitors, the average room occupancy rate increased by 19.9% (Figure 25) , and the room charges also increased (Schedule 14) . Total tax collected in the year was 59% more than that of the previous year (Figure 26) . |

| |

|

| |

| |

2003-04 |

2004-05 |

Increase |

| Hotels and Boarding Houses |

162 |

183 |

+13.0% |

| Taxable Rooms |

39,135 |

42,038 |

+7.4% |

| Exempted Rooms |

5,484 |

5,986 |

+9.2% |

|

| |

|

| |

| |

2003-04 |

2004-05 |

Increase |

| Room Days |

8,553,005 |

11,751,790 |

+37.4% |

| Occupancy Rate |

67.2% |

87.1% |

+19.9% |

|

| |

|

| |

|

|

|

| Tax Reserve Certificates |

| |

|

There are two sets of circumstances under which Tax Reserve Certificates are purchased.

The first applies to taxpayers who wish to save for the payment of their future tax liabilities. Two service schemes are offered to these taxpayers: the "Electronic Tax Reserve Certificates Scheme" for all taxpayers and the "Save-As-You-Earn" (SAYE) Scheme for civil servants and civil service pensioners. Under the Electronic Tax Reserve Certificates Scheme, certificates can be purchased using various electronic means, i.e. by bank autopay, telephone, the Internet, public information kiosk and bank ATM. Under the SAYE Scheme, certificates are purchased by civil servants and civil service pensioners through monthly deductions from their salaries/pensions. Interest is payable on the certificates when they are redeemed for settlement of tax liabilities, based on the interest rate prevailing at the time of purchase, for a maximum period of 36 months from the date of purchase.

In 2004-05, the number and amount of certificates sold under the SAYE Scheme decreased by 10% and 12% respectively (Schedule 15) . While there was a decrease of 51% in the number of certificates sold under the Electronic Tax Reserve Certificates Scheme, a single sizeable sale boosted the amount under the Scheme by 240% as compared with the previous year. The total amount of certificates sold increased by 157% (Figure 27) .

The second situation applies to taxpayers who object to tax assessments and are required to purchase Tax Reserve Certificates in respect of the tax in dispute. Such certificates are used to settle any tax found payable upon the finalisation of the objection or appeal. Interest is only payable on the amount, if any, subsequently required to be repaid to the taxpayer, and is computed at floating rates ruling over the tenure of the certificate. |

| |

|

| |

|

|

| |

| * A promotion campaign lodged by a payment service provider in 2003-04 has led to a substantial jump in the number of certificates sold under the Electronic Tax Reserve Certificates Scheme during the year. |

| |

|

| |

|

|

|

|