RSS

RSS  Share

Share Printer View

Printer View

Illustrative Examples

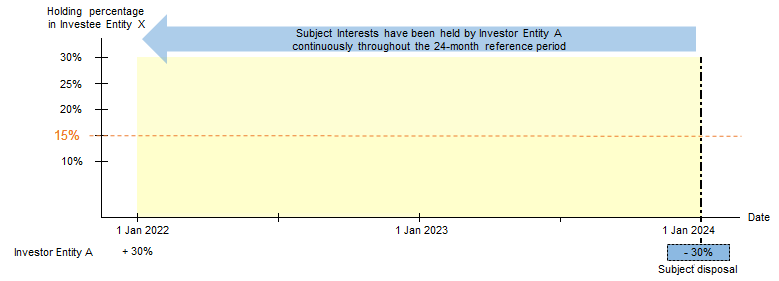

Scenario:

Investor Entity A is a private company carrying on a financing business in Hong Kong. On 1 January 2022, Investor Entity A acquired 30% of equity interests in Investee Entity X. Investee Entity X is engaged in the provision of consultancy services. On 1 January 2024, Investor Entity A disposed of 30% of equity interests in Investee Entity X and derived onshore gains from the disposal. The equity interests in Investee Entity X held by Investor Entity A have never been regarded as trading stock for tax purposes.

Reply:

"+" denotes acquisition of equity interests in Investee Entity X

"-" denotes disposal of equity interests in Investee Entity X

Investor Entity A has held 30% of equity interests in Investee Entity X (Subject Interests) throughout the continuous period of 24 months immediately before the date of the subject disposal (24-month reference period) (i.e. period from 1 January 2022 to 31 December 2023) and the Subject Interests by themselves constitute qualifying interests in Investee Entity X (i.e. at least 15% of equity interests in Investee Entity X). The equity holding conditions for the subject disposal of the Subject Interests are met and the onshore gains derived by Investor Entity A would be regarded as capital in nature and not chargeable to profits tax.

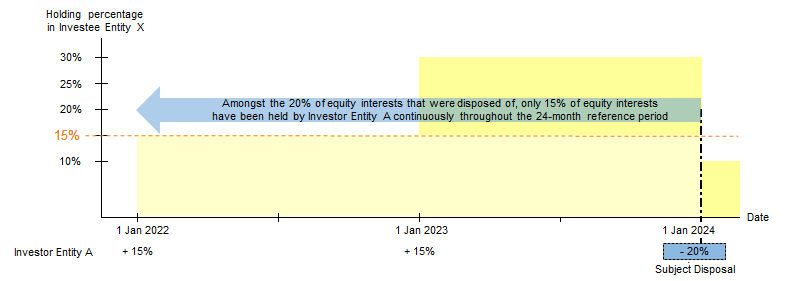

Scenario:

The facts are the same as those in Example 1, except that Investor Entity A acquired 15% of equity interests in Investee Entity X on 1 January 2022 and another 15% of equity interests in Investee Entity X on 1 January 2023. On 1 January 2024, Investor Entity A disposed of 20% of equity interests in Investee Entity X and derived onshore gains from the disposal.

Reply:

"+" denotes acquisition of equity interests in Investee Entity X

"-" denotes disposal of equity interests in Investee Entity X

The equity interests in Investee Entity X are taken to be disposed of by Investor Entity A on a first-in-first-out basis. Therefore, of the 20% of equity interests in Investee Entity X that were disposed of, the first 15% was acquired on 1 January 2022 and the remaining 5% was acquired on 1 January 2023. In view that only 15% of equity interests in Investee Entity X have been held throughout the continuous period of 24 months immediately before the date of the subject disposal (24-month reference period) (i.e. period from 1 January 2022 to 31 December 2023), the Scheme would only apply to the part of disposal gains arising from the disposal of the 15% of equity interests acquired on 1 January 2022.

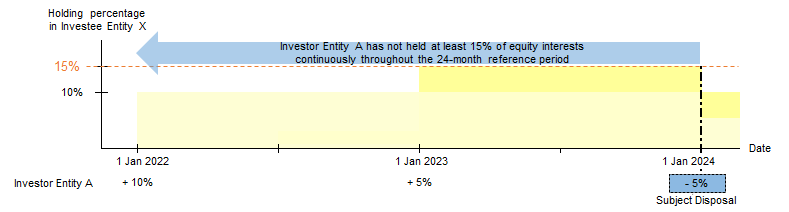

Scenario:

The facts are the same as those in Example 1, except that Investor Entity A acquired 10% of equity interests in Investee Entity X on 1 January 2022 and another 5% of equity interests in Investee Entity X on 1 January 2023. On 1 January 2024, Investor Entity A disposed of 5% of equity interests in Investee Entity X and derived onshore gains from the disposal.

Reply:

"+" denotes acquisition of equity interests in Investee Entity X

"-" denotes disposal of equity interests in Investee Entity X

The Scheme does not apply to the onshore gains derived from the subject disposal. This is because Investor Entity A has not held at least 15% of equity interests in Investee Entity X throughout the continuous period of 24 months immediately before the date of the subject disposal (24-month reference period) (i.e. period from 1 January 2022 to 31 December 2023). Whether the disposal gains are capital or revenue in nature would be determined based on a “badges of trade” analysis.

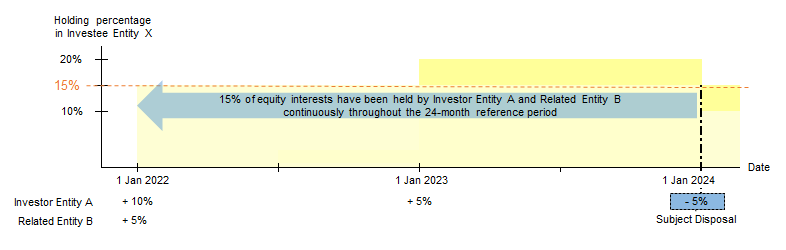

Scenario:

The facts are the same as those in Example 3. Assume further that Investor Entity A has a closely related entity, Related Entity B, in which Investor Entity A has held 60% of the beneficial interest. On 1 January 2022, Related Entity B acquired 5% of equity interests in Investee Entity X. Related Entity B has been a closely related entity of Investor Entity A throughout the whole period from 1 January 2022 to 1 January 2024 and the equity interests in Investee Entity X held by Related Entity B have never been regarded as trading stock for tax purposes.

Reply:

"+" denotes acquisition of equity interests in Investee Entity X

"-" denotes disposal of equity interests in Investee Entity X

Applying the first-in-first-out basis, 5% of equity interests in Investee Entity X acquired by Investor Entity A on 1 January 2022 (Subject Interests) are taken to be disposed of on 1 January 2024. Given that the Subject Interests, together with the other 5% of equity interests acquired by Investor Entity A on 1 January 2022 and 5% of equity interests acquired by Related Entity B on 1 January 2022, have been held throughout the continuous period of 24 months immediately before the date of the subject disposal (24-month reference period) (i.e. period from 1 January 2022 to 31 December 2023) and that the above equity interests, in aggregate, constitute 15% of equity interests in Investee Entity X, the equity holding conditions are met for the subject disposal. In this regard, the onshore gains derived by Investor Entity A from the subject disposal would be regarded as capital in nature under the Scheme.

In determining whether the condition on 15% holding threshold is met, provided that Related Entity B has been a closely related entity of Investor Entity A throughout the 24-month reference period, the direct equity interests in Investee Entity X held by Related Entity B (i.e. 5% of equity interests in Investee Entity X) would be taken into account for aggregation.

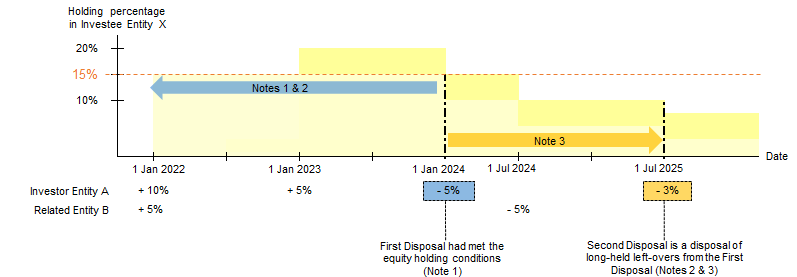

Scenario:

The facts are the same as those in Example 4. Subsequent to the disposal of 5% of equity interests in Investee Entity X by Investor Entity A on 1 January 2024 (First Disposal), Related Entity B disposed of 5% of the equity interests in Investee Entity X on 1 July 2024 and Investor Entity A further disposed of 3% of equity interests in Investee Entity X (Subject Interests) on 1 July 2025 (Second Disposal). Investor Entity A derived onshore gains from the Second Disposal.

Reply:

"+" denotes acquisition of equity interests in Investee Entity X

"-" denotes disposal of equity interests in Investee Entity X

| Note 1: | 15% of equity interests, including the disposed interests of 5%, have been held continuously throughout the 24-month reference period (i.e. from 1 Jan 2022 to 31 Dec 2023) |

| Note 2: | Subject interests under the Second Disposal had been held continuously throughout the 24-month reference period in relation to the First Disposal and constituted a part of the 15% of equity interests in relation to the First Disposal |

| Note 3: | Second Disposal occurs within 24 months after the First Disposal |

The equity holding conditions are not met for the Second Disposal since the holding percentage of equity interests in Investee Entity X held by Investor Entity A and Related Entity B immediately before the date of the Second Disposal is 10%, which is less than 15%. Despite this, the onshore gains derived from the Second Disposal would still be regarded as capital in nature under the Scheme on the basis that:

| (a) | before the Second Disposal, other equity interests in Investee Entity X had been disposed of by Investor Entity A (i.e. First Disposal); |

| (b) | the First Disposal had met the equity holding conditions and thus the onshore gains derived therefrom are regarded as capital in nature and not chargeable to profits tax; |

| (c) | the equity holding conditions for the First Disposal had been met on the basis that the Subject Interests had been held by Investor Entity A continuously throughout the 24-month reference period in relation to the First Disposal and constituted a part of the 15% of equity interests in Investee Entity X in relation to the First Disposal; and |

| (d) | the Second Disposal occurs within 24 months after the First Disposal. |

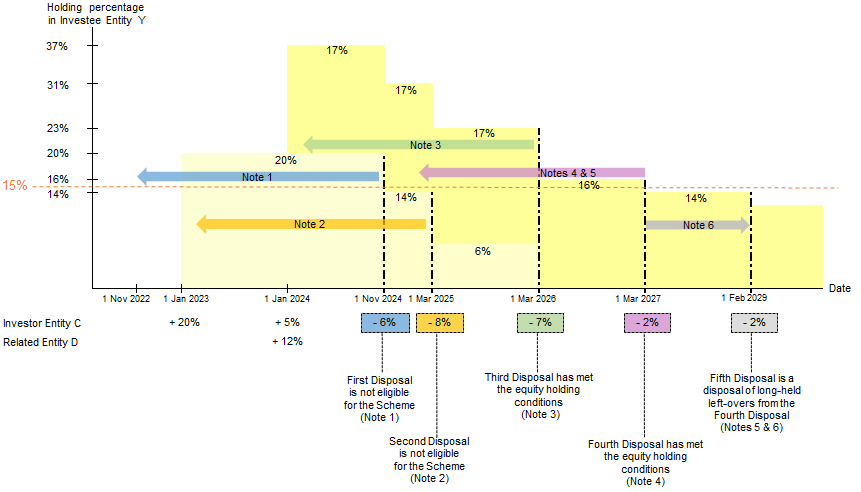

Scenario:

Investor Entity C is a partnership carrying on transportation business in Hong Kong. It has a closely related entity known as Related Entity D. On 1 January 2023, Investor Entity C acquired 20% of equity interests in Investee Entity Y, which is a publicly listed company. On 1 January 2024, Investor Entity C and Related Entity D acquired another 5% and 12% of equity interests in Investee Entity Y respectively. On the following dates, Investor Entity C disposed of its equity interests in Investee Entity Y and derived onshore gains from each of the disposals:

Disposal of 6% on 1 November 2024 (First Disposal)

Disposal of 8% on 1 March 2025 (Second Disposal)

Disposal of 7% on 1 March 2026 (Third Disposal)

Disposal of 2% on 1 March 2027 (Fourth Disposal)

Disposal of 2% on 1 February 2029 (Fifth Disposal)

Reply:

"+" denotes acquisition of equity interests in Investee Entity Y

"-" denotes disposal of equity interests in Investee Entity Y

| Note 1: | Subject interests under the First Disposal have been held for less than 24 months |

| Note 2: | Less than 15% of equity interests have been held throughout the 24-month reference period from 1 Mar 2023 to 28 Feb 2025 |

| Note 3: | At least 15% of equity interests, including the disposed interests of 7%, have been held continuously throughout the 24-month reference period from 1 Mar 2024 to 28 Feb 2026 |

| Note 4: | At least 15% of equity interests, including the disposed interests of 2%, have been held continuously throughout the 24-month reference period from 1 Mar 2025 to 28 Feb 2027 |

| Note 5: | Subject interests under the Fifth Disposal had been held continuously throughout the 24-month reference period in relation to the Fourth Disposal and constituted a part of the qualifying interests (i.e. at least 15% of equity interests) in relation to the Fourth Disposal. |

| Note 6: | Fifth Disposal occurs within 24 months after the Fourth Disposal |

First Disposal

The Scheme does not apply to the onshore gains derived from the First Disposal. This is because Investor Entity C has failed to hold the subject interests for a continuous period of 24 months immediately before the date of the First disposal (i.e. period from 1 November 2022 to 31 October 2024). The equity holding conditions for the First Disposal are not met. In this regard, whether the onshore gains derived from the First Disposal are capital or revenue in nature will be determined based on a “badges of trade” analysis.

Second Disposal

The Scheme does not apply to the onshore gains derived from the Second Disposal. This is because Investor Entity C has failed to hold at least 15% of equity interests in Investee Entity Y for a continuous period of 24 months immediately before the date of the Second Disposal (i.e. period from 1 March 2023 to 28 February 2025). Specifically, after the First Disposal of 6% of equity interests on 1 November 2024, the Investor Entity C’s equity interests in Investee Entity Y which have been held throughout the period since 1 March 2023 have dropped from 20% to 14% and thus, the equity holding conditions for the Second Disposal are not met. In this regard, whether the onshore gains derived from the Second Disposal are capital or revenue in nature will be determined based on a “badges of trade” analysis.

Subject to the condition that the disposed interests under the First Disposal and Second Disposal would not be regarded as trading stock under the “badges of trade” analysis, the Scheme would be applicable to the onshore gains derived from the Third Disposal, Fourth Disposal and Fifth Disposal on the following basis:

Third Disposal

Applying the first-in-first-out basis, of the 7% of equity interests in Investee Entity Y that were disposed of on 1 March 2026, 6% were acquired on 1 January 2023 and 1% were acquired on 1 January 2024. Given that the subject disposed interests, together with the other 4% of equity interests acquired by Investor Entity C on 1 January 2024 and 12% of equity interests acquired by Related Entity D on 1 January 2024, have been held throughout the continuous period of 24 months immediately before the date of the Third Disposal (i.e. period from 1 March 2024 to 28 February 2026) and that the above equity interests, in aggregate, constitute qualifying interests (i.e. at least 15% of equity interests) in Investee Entity Y, the equity holding conditions are met for the Third Disposal. In this regard, the onshore gains derived by Investor Entity C from the Third Disposal would be regarded as capital in nature under the Scheme.

Fourth Disposal

Applying the first-in-first-out basis, the 2% of equity interests in Investee Entity Y that were disposed of on 1 March 2027 were acquired on 1 January 2024. On the basis that the subject disposed interests, together with the remaining 2% of equity interests acquired by Investor Entity C on 1 January 2024 and 12% of equity interests acquired by Related Entity D on 1 January 2024, have been held throughout the continuous period of 24 months immediately before the date of the Fourth Disposal (i.e. period from 1 March 2025 to 28 February 2027) and that the above equity interests, in aggregate, constitute at least 15% of equity interests in Investee Entity Y, the equity holding conditions are met for the Fourth Disposal. In this regard, the onshore gains derived by Investor Entity C from the Fourth Disposal would be regarded as capital in nature under the Scheme.

Fifth Disposal

The equity holding conditions for the Fifth Disposal are not met since the holding percentage of equity interests in Investee Entity Y by Investor Entity C and Related Entity D immediately before the date of the Fifth Disposal is 14% which is less than 15%. Despite this, the onshore gains derived from the Fifth Disposal would still be regarded as capital in nature under the Scheme on the basis that:

| (a) | before the Fifth Disposal, other equity interests in Investee Entity Y had been disposed of by Investor Entity C (i.e. Fourth Disposal); |

| (b) | the Fourth Disposal had met the equity holding conditions and the onshore gains derived therefrom are regarded as capital in nature and not chargeable to profits tax; |

| (c) | the equity holding conditions for the Fourth Disposal had been met on the basis that the disposed interests under the Fifth Disposal had been held by Investor Entity C throughout the continuous period of 24-month reference period in relation to the Fourth Disposal and constituted a part of the qualifying interests (i.e. at least 15% of equity interests) in Investee Entity Y in relation to the Fourth Disposal; and |

| (d) | the Fifth Disposal occurs within 24 months after the Fourth Disposal. |

Scenario:

On 1 January 2023, Investor Entity E acquired 80% of the issued share capital in Investee Entity Z. Investee Entity Z was incorporated as a private company in Hong Kong and closes its accounts on 31 December every year. At all relevant times, Investee Entity Z does not carry on a business of property trading or property development and it wholly owns the following immovable properties in Hong Kong and outside Hong Kong:

| Immovable properties | Usage |

| Property A in Hong Kong | Held for own office use |

| Property B in Hong Kong | Held for rental income |

| Property C outside Hong Kong | Vacant (Note 1) |

Note 1: Assuming that Property C is an investment property of Investee Entity Z with which Investee Entity Z intends to hold for rental income and/or for capital appreciation at all relevant times. Nevertheless, at the end of the year 2024, Investee Entity Z planned to dispose of Property C for investment reasons and Property C had been left vacant before Investor Entity E disposed of the equity interests in Investee Entity Z.

On 1 July 2025, Investor Entity E disposed of all the equity interests in Investee Entity Z and derived an onshore gain. The financial accounts of Investee Entity Z gave the following details:

| As at | Total value of Investee Entity Z’s assets | Net book value of Property A | Fair value of Property B | Fair value of Property C |

| 31.12.2024 | $200m | $35m | $45m | $60m |

| 31.12.2025 | $300m | $30m | $50m | $70m |

Reply:

In determining whether Investee Entity Z is an excluded entity under the Scheme, it is necessary to calculate whether its immovable properties holding (i.e. the percentage of value of the specified immovable properties held by Investee Entity Z out of its total assets) in the basis period for the year of assessment in which the disposal occurs (i.e. from 1 January 2025 to 31 December 2025) exceeds 50%. Since Property A and Property B are used by Investee Entity Z to carry on its trade or business, the value of Property A and Property B could be carved out from the numerator in computing the percentage:

| ($60m + $70m) ÷ 2 | x 100% = 26% |

| ($200m + $300m) ÷ 2 |

In view that Investee Entity Z’s immovable property holding in the relevant basis period does not exceed 50%, Investee Entity Z would not be regarded as an excluded entity under the Scheme. The gains derived from the disposal of equity interests in Investee Entity Z would be regarded as capital in nature and not chargeable to profits tax if the specified conditions are met.

Alternatively, if Investor Entity E is able to provide the interim financial accounts of Investee Entity Z which were made up to the period ended 30 June 2025 or a valuation report to support the fair value of Property C at the time of the disposal, Investor Entity E can elect to compute the above percentage by reference to the fair value of Property C at the time of the disposal.

Scenario:

The facts are the same as those in Example 7. Assume further that Investee Entity Z holds 50% of the issued share capital in Entity F which holds 80% of the issued share capital in Entity G at all relevant times. Entity F and Entity G both hold an immovable property outside Hong Kong for sale respectively. With reference to the available financial accounts of Entity F and Entity G, the fair value of the respective immovable property is as follows:

| As at | Fair value of Property D held by Entity F | Fair value of Property E held by Entity G |

| 31.12.2024 | $100m | $30m |

| 31.12.2025 | $120m | $40m |

The value of direct and indirect beneficial interest of Investee Entity Z in Entity F and Entity G respectively that is attributable to the specified immovable property held by Entity F and Entity G is computed as follows:

| As at | Value of direct beneficial interest of Investee Entity Z in Entity F that is attributable to Property D | Value of indirect beneficial interest of Investee Entity Z in Entity G that is attributable to Property E |

| 31.12.2024 | $100m x 50% = $50m | $30m x 50% x 80% = $12m |

| 31.12.2025 | $120m x 50% = $60m | $40m x 50% x 80% = $16m |

In computing the percentage of value of the specified immovable properties held by Investee Entity Z out of its total assets in the relevant basis period (i.e. from 1 January 2025 to 31 December 2025), in addition to the value of Property C directly held by Investee Entity Z, the value of the direct or indirect beneficial interests of Investee Entity Z in Entity F and Entity G to the extent to which the value is attributable to immovable properties held by Entity F and Entity G are included in the numerator:

| [($60m + $70m)÷2] + [($50m + $60m)÷2] + [($12m + $16m)÷2] | x 100% = 53.6% |

| ($200m + $300m)÷2 |

In view that Investee Entity Z’s immovable property holding in the relevant basis period exceeds 50%, Investee Entity Z would be regarded as an excluded entity. The Scheme is not applicable to the gains derived from the disposal of equity interests in Investee Entity Z.

Alternatively, if Investor Entity E is able to provide the interim financial accounts of Entity F and Entity G which were made up to the period ended 30 June 2025 or a valuation report to support the fair value of Property D and Property E at the time of the disposal, Investor Entity E can elect to compute the above percentage by reference to the fair value of the relevant properties at the time of the disposal.