RSS

RSS  Share

Share Printer View

Printer View

![]()

1.

Q:

Mr. Chan and his spouse have following businesses:

| Business | Issued share capital/ voting rights/ profits entitled | |

| Mr. Chan | Mrs. Chan | |

| Corporation A | 50% | 50% |

| Corporation B | 50% | 50% |

| Partnership C | 60% | 40% |

| Sole Proprietorship D | 100% | -- |

| Sole Proprietorship E | -- | 100% |

| Sole Proprietorship F | -- | 100% |

Note: All the above businesses adopt the same basis period for a year of assessment.

A:

Corporation A and Corporation B are not connected entities as neither Mr. Chan nor Mrs. Chan has control over them. Both Corporation A and Corporation B qualify for the two-tiered profits tax rates.

Partnership C and Sole Proprietorship D are connected entities as Mr. Chan has control over them. Either Partnership C or Sole Proprietorship D can elect two-tiered profits tax rates in Partnership C's Profits Tax Return or Mr. Chan's Tax Return – Individuals.

Sole Proprietorship E and Sole Proprietorship F are also connected entities as they are sole proprietorship businesses carried on by Mrs. Chan. In her Tax Return – Individuals, Mrs. Chan can elect two-tiered profits tax rates for Sole Proprietorship E or Sole Proprietorship F.

![]()

2.

Q:

Mr. Lee and his family members have following businesses:

| Business | Issued share capital/ voting rights/ profits entitled | |||

| Mr. Lee | Mrs. Lee | Brother of Mr. Lee |

Son of Mr. & Mrs. Lee |

|

| Corporation A | 40% | 60% | -- | -- |

| Corporation B | 40% | -- | 60% | -- |

| Corporation C | -- | -- | 70% | 30% |

| Partnership D | 80% | -- | 20% | -- |

| Sole Proprietorship E | 100% | -- | -- | -- |

| Sole Proprietorship F | -- | 100% | -- | -- |

Note: All the above businesses adopt the same basis period for a year of assessment.

A:

Partnership D and Sole Proprietorship E are connected entities as Mr. Lee has control over them. Either Partnership D or Sole Proprietorship E can elect two-tiered profits tax rates in Partnership D's Profits Tax Return or Mr. Lee's Tax Return – Individuals.

Corporation A and Sole Proprietorship F are connected entities as Mrs. Lee has control over them. Either Corporation A or Sole Proprietorship F can elect two-tiered profits tax rates in Corporation A's Profits Tax Return or Mrs. Lee's Tax Return – Individuals.

Corporation B and Corporation C are connected entities as the brother of Mr. Lee has control over them. Only either Corporation B or Corporation C can elect two-tiered profits tax rates in its Profits Tax Return.

Corporation A and Partnership D are not connected entities even Corporation A is controlled by Mrs. Lee and Partnership D is controlled by Mr. Lee.

![]()

3.

Q:

Mr. Wong and Corporation H hold corporations and trust as follows:

| Business | Issued share capital/ voting rights | |

| Corporation H Note | Mr. Wong | |

| Corporation A | 100% | -- |

| Corporation B | 60% | 40% |

| Corporation C | 50% | 50% |

| Corporation D | 30% | 70% |

| Trust T | -- | Mr. Wong as trustee |

Note: Mr. Wong does not own any issued share capital and voting rights in Corporation H.

A:

Corporation H, Corporation A and Corporation B are connected entities. Only one of them can elect two-tiered profits tax rates.

Corporation C has no connected entity and qualifies for two-tiered profits tax rates.

Trust T is not a connected entity of Corporation D as Mr. Wong does not have control over Trust T solely by acting in the capacity of a trustee.

![]()

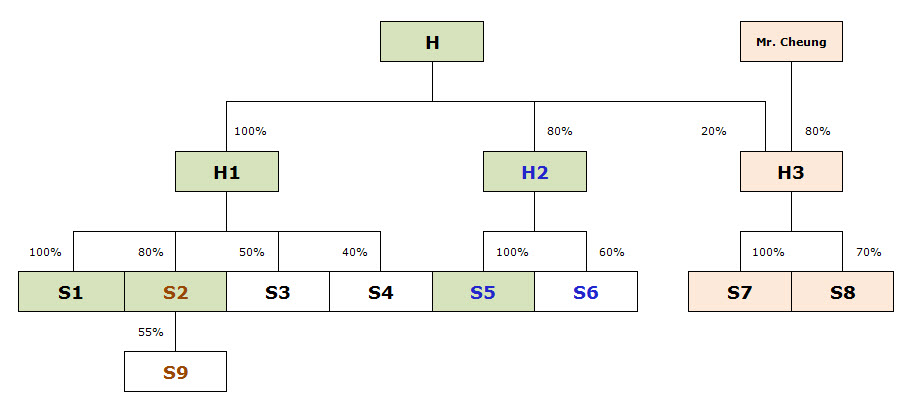

4.

Q:

Group companies

Mr. Cheung and Corporation H hold corporations as follows:

A:

| Business | Issued share capital/ voting rights (directly or indirectly) |

|

| Corporation H | Mr. Cheung | |

| Corporation H1 | 100% | -- |

| Corporation S1 | 100% | -- |

| Corporation S2 | 80% | -- |

| Corporation S3 | 50% | -- |

| Corporation S4 | 40% Note 1 | -- |

| Corporation H2 | 80% | -- |

| Corporation S5 | 80% Note 2 | -- |

| Corporation S6 | 48% Note 3 | -- |

| Corporation H3 | 20% | 80% |

| Corporation S7 | 20% | 80% Note 4 |

| Corporation S8 | 14% Note 5 | 56% Note 6 |

| Corporation S9 | 44% Note 7 | -- |

| Notes: | |

| (1) | The remaining 60% shareholding in Corporation S4 is held by shareholders each holding not more than 10% of the issued share capital. |

| (2) | Corporation H owns or controls 80% (i.e. 80% x 100%) in aggregate of the issued share capital / is entitled to exercise or controls the exercise of 80% in aggregate of the voting rights in Corporation S5. |

| (3) | Corporation H owns or controls 48% (i.e. 80% x 60%) in aggregate of the issued share capital / is entitled to exercise or controls the exercise of 48% in aggregate of the voting rights in Corporation S6. |

| (4) | Mr. Cheung owns or controls 80% (i.e. 80% x 100%) in aggregate of the issued share capital / is entitled to exercise or controls the exercise of 80% in aggregate of the voting rights in Corporation S7. |

| (5) | Corporation H owns or controls 14% (i.e. 20% x 70%) in aggregate of the issued share capital / is entitled to exercise or controls the exercise of 14% in aggregate of the voting rights in Corporation S8. |

| (6) | Mr. Cheung owns or controls 56% (i.e. 80% x 70%) in aggregate of the issued share capital / is entitled to exercise or controls the exercise of 56% in aggregate of the voting rights in Corporation S8. |

| (7) | Corporation H owns or controls 44% (i.e. 100% x 80% x 55%) in aggregate of the issued share capital / is entitled to exercise or controls the exercise of 44% in aggregate of the voting rights in Corporation S9. |

Corporations H, H1, H2, S1, S2 and S5 are connected entities as Corporation H has control, either directly or indirectly, over the other entities. Only one of them can elect two-tiered profits tax rates.

Corporation S6 is a connected entity of Corporation H2 and Corporation S5. Corporation S6 can elect two-tiered profits tax rates if Corporation H2 and Corporation S5 do not elect.

Corporation S9 is a connected entity of Corporation S2. Corporation S9 can elect two-tiered profits tax rates if Corporation S2 does not elect.

Corporation H3, Corporation S7 and Corporation S8 are also connected entities. Only one of them can benefit from two-tiered profits tax rates.

Corporation S3 and Corporation S4 do not have connected entity and they both qualify for the two-tiered profits tax rates.