RSS

RSS  Share

Share Printer View

Printer View

Tips for tagging

Finding the closest available tag

You are advised to look for the closest available tag of an accounting or tax item not just from the elements grouped under the heading concerned. You should also consider elements under other headings where appropriate. For example, where there is an element, “Amount due to a director” in the Statement of financial position, you may not find the appropriate tag under the group [210000] Statement of financial position, current/non-current or [220000] Statement of financial position, order of liquidity. Rather, you may consider the tag “Current payables/loans from directors” under the group [800100] Notes - Subclassifications of assets, liabilities and equities more appropriate.

Elements are grouped under headings in Taxonomy illustrated in excel to facilitate searching and for your reference. The same element may appear under different groups / headings. For example, ‘Property, plant and equipment’ under the headings [210000] Statement of financial position, current/non-current and [220000] Statement of financial position, order of liquidity are the same element. It is not necessary for you to consider whether they are different items and make efforts to choose the better one.

Consistency of data values for a single fact

The same piece of numeric fact MUST NOT BE reported with different data values unless the fact is reported at different rounding levels. The purpose is to minimize confusion arising from tags of a single fact containing inconsistent values. Values tagged in different sections of the financial statements or tax computations for the same period must be consistent as they are rounded from a single value. For example, the revenue for current year of $100,000 may appear in both Statement of comprehensive income, profit or loss and notes to the financial statements. You can use the same tag ‘Revenue’ with same attributes to tag this value repeatedly, but you must ensure that the facts to be tagged are all $100,000 and referred to the revenue for current year.

Generally, financial statements contain comparative figures of last year. At the initial stage, the Department does not require you to submit the previous year’s figures but you are encouraged to tag those comparative figures. An appropriate period attribute should be assigned when tagging the comparative figures. Following the example above, the tag ‘Revenue’ with period attribute year 2 will be used to tag $100,000 while the same concept ‘Revenue’ with period attribute year 1 will be used to tag the last year’s revenue, say $90,000. Such tagging does not violate the consistency of data values for duplicate fact described above as the attributes of the tag are not the same.

Information required by Profits Tax returns

As stipulated in Notes and Instructions of Profits Tax returns (forms BIR51 and BIR52), you are required to submit certain detailed information for a tax data. For example, in respect of commission paid, you are required to provide the Department with details of each recipient including name, address and Hong Kong Identity Card Number or Business Registration Number, amount paid and nature of service. You have to tag such information in the tax computations as required.

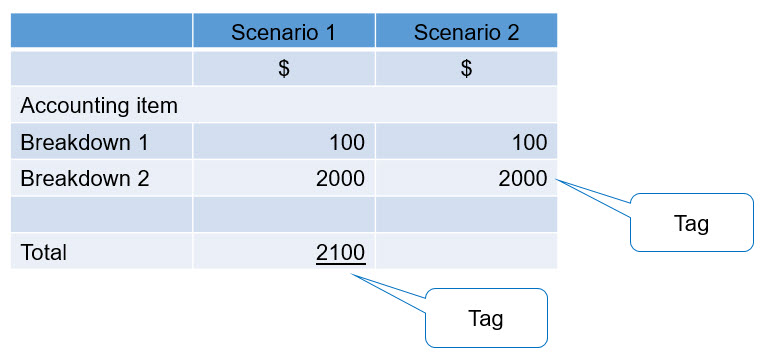

As stated above, a single tag with same attribute should not be used to tag different facts. Businesses may provide both breakdown and total, or either one for an accounting item in their financial statements. You should tag the total figure if it is available (see Scenario 1 in the below illustrative example). In case the breakdown is only provided but not the total, the greatest value of the breakdown should be tagged (see Scenario 2 in the below illustrative example).

Example: